The title is taken from a recent Bloomberg article from Jessica Nix to whom I provided some background information, so I thought I should respond to some of the issues raised by this piece.

The yachting industry offers significant economic and experiential benefits, but in the face of a climate emergency, were the IPCC state every ton of CO2 matters, this cannot be used as an excuse for business as usual. Climate change is not new, and there has been plenty of time for the industry to adjust to a more responsible model.

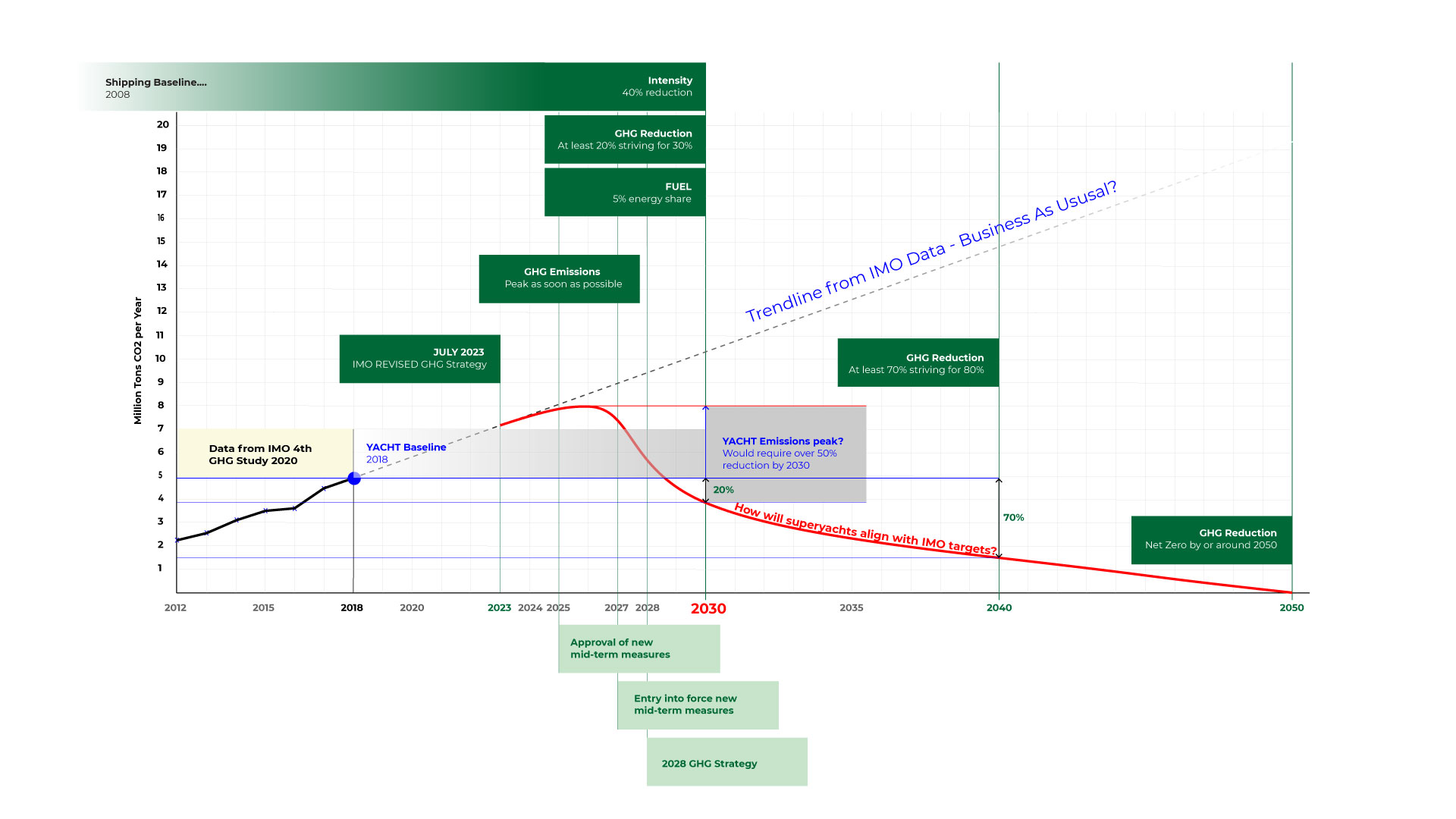

Shipping is progressing at an accelerating pace due to IMO regulations related to decarbonisation (not applicable to yachts) and EU Carbon Tax on Shipping (not applicable to yachts except commercial yachts ≥5000GT) as well as commercial pressure from customers and lenders. These are externalities that have resulted in operational changes, efficiency drives and a switch to alternative fuels.

According to DNV, the percentage of vessels being built to run on alternative fuels.

- 16% of all vessels on order

- 21% of orders in the last 12 months, with Methanol overtaking LNG

Boat International Design Festival 2024

According to the Boat International Global Order Book (GOB) projects broken down into modes of propulsion.

- Diesel 1084

- Hybrid 41

- Diesel Electric 34

- Electric 10

I find these figures striking and disappointing, especially given how much shipyards, and the superyacht media, have been promoting the benefits of hybrid.

And whilst there are yachts from forward thinking builders like Feadship, Luerssen, San Lorenzo and Ferretti Group, that will use Hydrogen in their energy mix, either in pure form, or reformed from Methanol, as well as the much-anticipated Project Zero sailing yacht, these remain outliers – less than 0.5% of current projects.

There is also a growing number of yachts adding solar panels to the energy mix, however it should be noted that, in the main, they provide only a tiny amount of a yachts overall energy demand.

In total, over 99% of the GOB are diesel powered (though some are also #HVO ready) which does not seem to fit well with the claim often made we are the Formula 1 of the maritime industry.

I understand the slow pace due to availability of Green Hydrogen or Green Methanol, but HVO, a renewable diesel that can significantly reduce CO2 and other pollutants, is also experiencing low uptake. Education and availability play a part, but the biggest factor is price, with owners unwilling to pay for the higher priced fuel to support this most exceptional lifestyle.

And “fuel” also includes shore power. The CO2 intensity of electricity varies considerably, from around 56 gCO2/kWh in France (Our World in Data 2023) due to the low carbon energy mix, to 376 gCO2/kWh in places like Florida (US Energy Information Association) where the majority comes from fossil fuels. By comparison a diesel generator emits around 600 gCO2e/kWh at optimum load.

I am also conscious it is not only about the energy carrier, but also production and materials, operational efficiencies and other technical improvements, such as improved hull dynamics, more efficient air conditioning, the use of waste heat, etc., all of which are important in helping to improve the environmental impact.

Admittedly, yachting CO2 emissions are tiny compared to other industries, but when you break it down on a per capita basis, it is clearly disproportionate.

According to evidence, our emissions are growing, though we simply have no idea because we do not collect the data…a bizarre act of exceptionalism and self-harm.

This growth in emissions is mainly due to the growth of the fleet, accelerated by the recent boom, and also by the fact superyachts have an extended life compared to commercial ships – very few are taken out of service or scrapped. Yachts are also travelling further afield. Without significant change, the emissions from superyachts could easily exceed 10 Mt CO2 annually in 2030 – up from 4.7 Mt CO2 in 2018 (IMO GHG Study 2020).

To put this in context; if superyachts were a country their CO2 emissions would place them about 110 out of 211 countries – https://edgar.jrc.ec.europa.eu/report_2022 – this is clearly not sustainable.

I understand the defense of superyacht’s and their Owners, it’s an amazing industry but the truth is that we are not unique. All businesses and individuals have a responsibility to reduce their CO2 emissions and, arguably, those individuals who emit the most and have the financial means to reduce them, should be making the deepest cuts?

We are not short of solutions, but it seems the lack of external factors like regulation and/or carbon taxes – reputational damage might be a growing concern to some – and data driven accountability, is hindering progress.

No doubt cost is a consideration, but there is a short sightedness on this topic. The capital outlay may be higher for a more energy efficient yacht and the return on investment (ROI) difficult to justify on reduced operational expenses (OPEX) during the short ownership cycle. However, the higher cost should be viewed in the context of future risks such as regulations and taxes and the impact on resale value – possibly within the build time!

A handful of innovative projects though important and provide optimism, are not representative of the wider industry – as suggested by the GOB. For long-term survivability the yachting industry must do better including, energy efficient yachts becoming the norm, an accelerated switch from fossil diesel, real evidence – data! – of positive change, and an industry wide commitment to a more sustainable future.